In the latest PrOPEL Hub blog, Tim Butcher, Chief Economist and Deputy Secretary at the Low Pay Commission and Dr Imelda McCarthy, Research Fellow and Organisational Psychologist at CRÈME, consider how increases in the National Living Wage and the Covid-19 pandemic will impact small and microbusinesses and outline opportunities to join the Low Pay Commission microbusiness forum.

The Low Pay Commission (LPC) is an independent public body that advises the Government about the National Living Wage (NLW) and the National Minimum Wage (NMW). Each year, it makes its recommendations on increases in the minimum wage rates based on wide consultation, including seeking input from employers of all sizes of business, and in-depth research and analysis of the labour market with a focus on low-paying sectors and low-paid workers, which it publishes in its Annual Report.

The LPC and CREME have a longstanding relationship and have worked together on various research projects. Most recently the LPC acts as an advisor on CREME’s ESRC Productivity from Below project, which seeks to provide a detailed understanding of management and engagement practices and their relationship to productivity in microbusinesses from the catering, creative and retail sector. Here we focus on two aspects of the LPC’s Annual Report that are significant to this project: (1) proposed NLW increases, with an invite to microbusinesses to join an LPC forum, and (2) the economic impact of the Covid-19 pandemic on small and micro businesses. Direct extracts are taken from the report

The National Living Wage

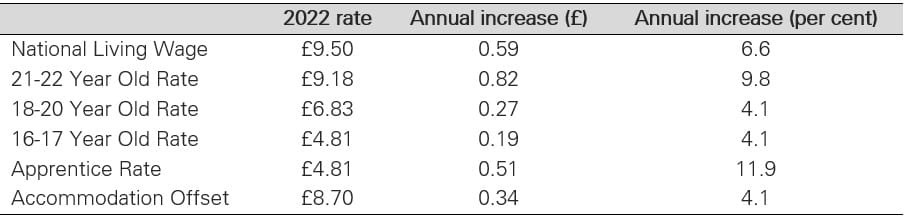

This year’s report sets out recommendations for the NLW and other minimum wage rates to be applied from April 2022 (see blog reassigned Table 1), this includes a 6.6% increase in the NLW (an increase of 59 pence) to £9.50. Similar increases are expected over the next two years if this target is met (see Table 10.1)

It is recognised that businesses deal with wage increases in a variety of ways, including altering employment hours, adjusting non-wage aspects of pay, changing pay structures, squeezing profits, increasing prices, and improving productivity. Considering this, the LPC is keen to understand the difference between how small and large businesses respond to increases in the minimum wage and want to build their evidence base accordingly.

Consultation opportunity: The LPC is keen to work with microbusinesses and would like to establish a forum to gather evidence to help guide future action on the implementation of the NLW and other minimum wage recommendations, particularly from those representing ethnic minority businesses and/or low-pay sectors. Forum members would be invited to interact with the LPC in a variety of ways, including written communication, individual consultation, and/or group events. A selection of the types of organisations already collaborating with the LPC can be found in Appendix 1 (p.199) of the Annual Report (note some consultees have opted to remain anonymous and are not included in the list). Expressions of interest can be made via CREME (details below).

The economic impact of the Covid-19 pandemic on small and micro businesses

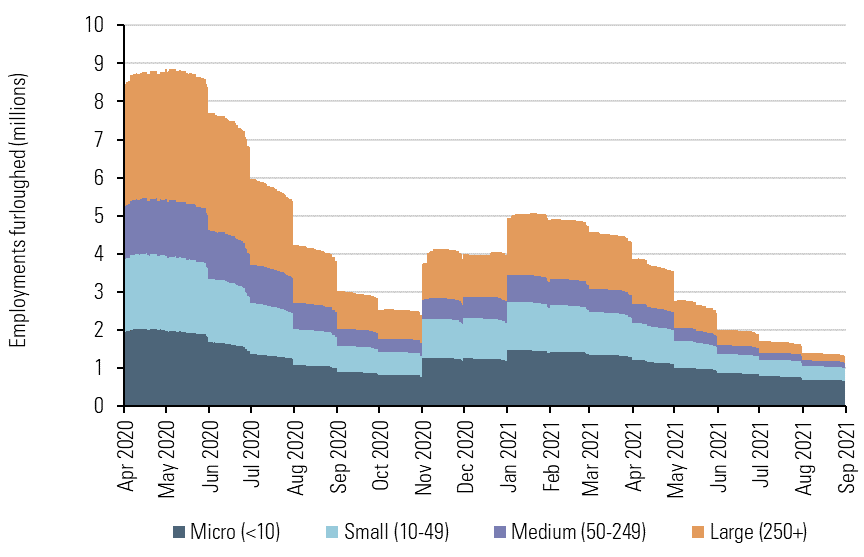

Covid-19 restrictions saw substantial uptake in the UK’s Coronavirus Job Retention Scheme from businesses of all sizes, but whilst the easing of restrictions contributed to a reduction in uptake by larger businesses (with 250+ employees), to fewer than 200,000 employments, this was not the case for small (with 10-49 employees) and micro firms (with <10 employees) who represented the majority proportion of the 1.3 million workers on furlough when the scheme ended in September 2021. Notable too was the relatively consistent level of uptake for the duration of the furlough scheme amongst microbusinesses compared to their larger counterparts (see Figure 2.15b).

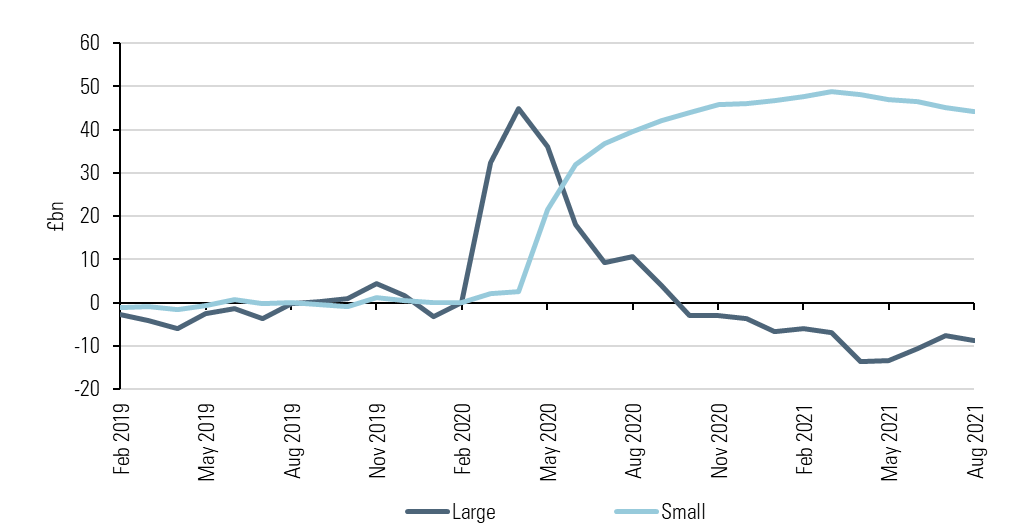

Receptiveness to Government-backed loans or finance was another area that saw variation according to organisational size. The ONS Business Insights and Conditions Survey (BICS) revealed small firms were more likely than micro (who similarly are less likely to have cash reserves) and large firms to take on debt, despite relatively low levels of debt accumulation pre-pandemic. Indeed, there was a marked difference between small and large firms (see Figure 9.4).

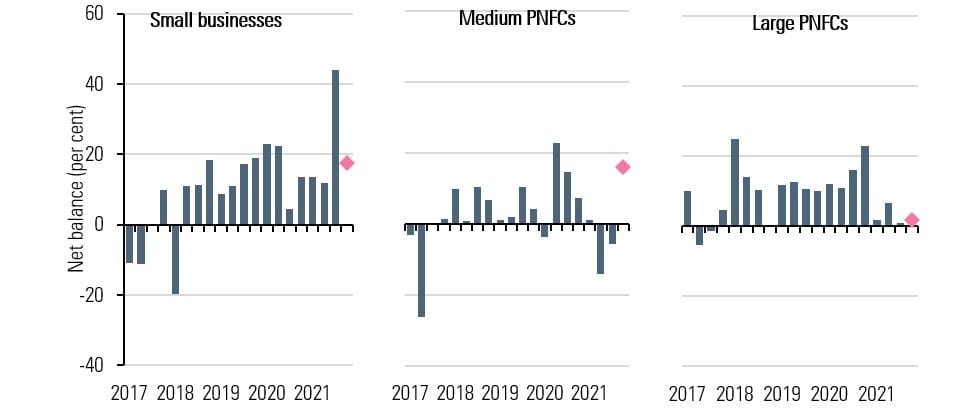

At the start of the pandemic (February to April 2020) large firms were at the forefront when it came to accessing loans (with debt rising to £45 billion), however this peak was temporary, with rates returning to pre-pandemic levels by October 2020. In contrast the introduction of Bounce Back Loans in May 2020 saw a rise in small firms accessing loans, however this level of debt has remained high (£44 billion at the end of August 2021) despite the economy reopening. Lenders are now concerned about the likelihood of defaults on loan repayments amongst small and medium-sized firms. Such concerns were elevated for small firms in the third quarter of 2021, in comparison to large firms who prompted close to zero concern at the same timepoint (see Figure 9.5).

Contact Us

To express an interest in joining the LPC microbusiness forum or to find out more information contact the Centre, email Gurdeep Chima (CREME Centre Manager), at [email protected]

Tables

Blog reassigned Table 1: The NLW and other minimum wage rates (p. xxvi Annual Report)

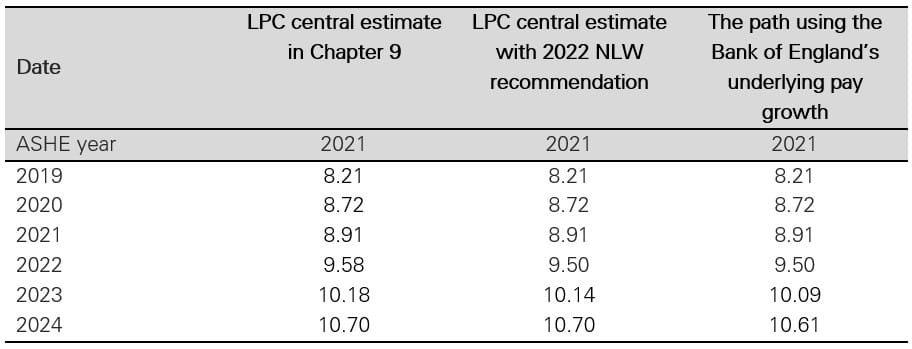

Table 10.1: The NLW path including our 2022 recommendation

Source: LPC estimates using ASHE 2010 methodology, April 2021, loss of pay furloughed weights. Forecasts are based on growth in AWE total pay (KAB9) from HM Treasury (2021a and 2021b) and the Bank of England (2021c).

Notes:

- The LPC central estimate is as set out in Chapter 9. The methodology for the projection of the path is given in the notes to Table 9.4.

- The LPC central estimate with 2022 NLW recommendation sets the 2022 NLW at £9.50. The path is then recalibrated form there using the median of wage forecasts.

- The final column uses the Bank of England’s underlying pay growth for April 2021 to April 2022 but imposes the NLW to be £9.50 in 2022. It has a weaker path for median hourly pay than our central estimate.

Figure 2.15b: Employments furloughed by age and firm size, UK, April 2020 – August 2021

Source: LPC estimates using HMRC CJRS data, UK, 1 Apr 2020-31 Aug 2021.

Figure 9.4: Level of firm debt relative to February 2020, by size of firm, UK, 2019-2021

Source: LPC estimates using Bank of England series Z8YI and Z8YH (Monthly amounts outstanding of monetary financial institutions’ sterling and all foreign currency loans to large and small businesses), UK, February 2019-August 2021.

Figure 9.5: Net percentage balance for changes in default rates on loans to firms, by size, UK, 2017-2021

Source: Bank of England (2021g). Credit Conditions Survey 2021 Q3. Chart 6, 2017-2021.

Note: Question: ‘How has the default rate on loans to small/medium/large PNFCs changed?’ Net percentage balances are calculated by weighting together the responses of those lenders who answered the question. The blue bars show the responses over the previous three months. The pink diamond shows the expectation over the next three months. A positive balance indicates an increase in the default rate.